What is consultant insurance?

Consultant insurance isn’t just one product; it is a package that comprises several products designed to meet the specific needs of your consulting business.

Given the advisory nature of consulting work, professional indemnity insurance should be one of the first covers you look to get. Consultants may also need public liability if they are working face-to-face with clients. Portable electronics insurance can be helpful if you travel with expensive computer equipment.

Why do consultants need insurance?

Your work with clients may not always go to plan, and if your recommendations don’t yield the expected results, your client may want answers. In these situations, discussions can get heated and sometimes escalate into accusations against you or disputes over money or compensation.

Accusations of making a professional mistake

Professional mistakes by consultants can result in adverse outcomes for clients, including loss of earnings, additional spending to rectify an error or reputational damage. If your client believes your work led to the problem, they may take legal action against you.

Blame for causing a financial loss

If you are blamed for causing your client financial loss, you may end up in court proceedings. If you don’t have adequate insurance to cover the claim, you may find your business or personal assets on the line.

Contract disputes

Unmet expectations or poorly defined project scope are common causes of contract disputes. These disputes may result in unpaid invoices or your needing to do additional work due to scope creep.

Unpaid invoices

More often than not, consultants have to deal with bad debt. Customers either unduly delay payments or try to avoid paying your fees altogether.

Professional indemnity insurance for consultants

Providing advice is a consultant’s primary role; this is why professional indemnity insurance is the most helpful cover for independent consultants.

Professional indemnity is a legal cover that insures consultants against legal accusations of professional mistakes, negligence, breach of confidentiality, and more. It pays the associated cost of legal defence and will pay any compensation if you are found liable.

The exposures consultants face are often substantial should something go wrong, and professional indemnity provides an affordable safety net.

What does consultant professional indemnity insurance cover?

Professional indemnity protects consultants from claims or accusations of wrongdoing from their professional advice or work product.

Cover includes:

- Giving the wrong advice or recommendation

- Making a mistake

- Acting negligently

- Confidentiality breaches

For example, a client may claim:

- The information you shared about their business was confidential and caused a financial loss

- Your recommendations ended up losing your client’s business money

- Your work wasn’t up to the expected standards, and your client is asking for a financial remedy

- A party you contracted didn’t fulfil their contractual obligations, failing the client’s project, and the client is now seeking compensation from you.

How much professional indemnity does a consultant need?

When getting professional indemnity insurance in the UK, coverage limits vary greatly, from £50,000 to millions. The provider pays only up to the limit in the event of a claim.

To ensure adequate coverage, identify the appropriate limit based on factors like your work, client size, and contracts. Your client contract will normally specify a liability limit, so get a policy that matches or exceeds that amount.

Does professional indemnity insurance cover my consultant activities worldwide?

Your professional indemnity policy's ‘territory or geographical limits’ and ‘jurisdiction’ sections specify if your life coach insurance will respond when working in different countries.

Territory or geographical limits:

The territory or geographical limit specifies where you can virtually or physically deliver your services. For example: “Worldwide.”

Jurisdictional limit:

The jurisdictional limit specifies which legal jurisdictions your policy will defend you if you are sued. For example: “Worldwide excluding US and Canada.”

Contract governance:

Any contracts or agreements you enter into with your clients should specify the ‘governing law’ for that contract, which is the jurisdiction in which parties can seek legal remedy for breach of contract.

Avoid entering contracts not governed by your local jurisdiction and/or excluded by your life coaching professional indemnity insurance.

If you work with US and Canadian clients, you can reduce your risk by not entering contracts governed by US and Canadian laws.

Switching your professional indemnity insurance

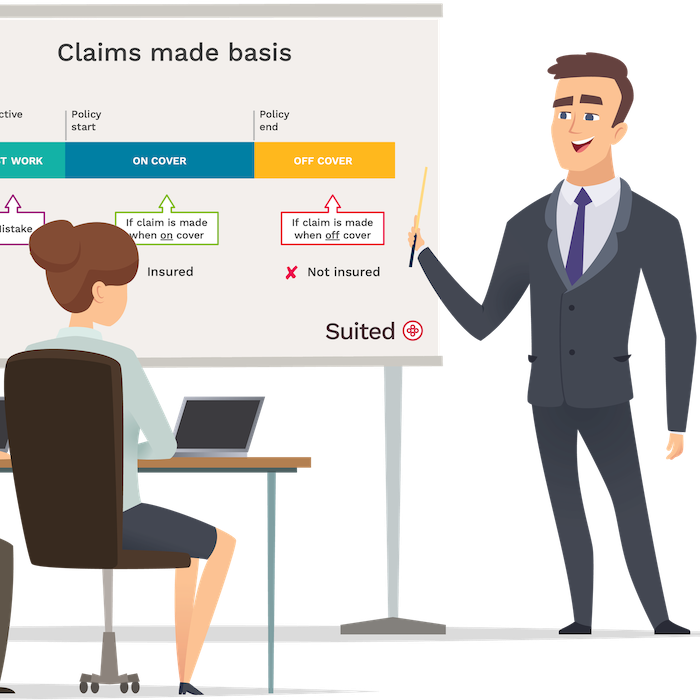

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your consultant insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I have professional indemnity if I am between contracts?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from consulting. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of consulting you did and the likelihood that a client might bring a claim against you.

Public liability insurance for consultants

If you frequently meet with clients in person or work at their location, it is recommended to obtain public liability insurance. This type of insurance can shield you from claims of causing an accident that resulted in injury or damage to property.

Having public liability insurance can be an affordable way to protect yourself against unforeseen incidents like slips, falls, or accidentally causing harm to someone else's property. While the compensation for public liability claims is usually not significant, legal defence expenses can accumulate quickly.

What does consultant public liability insurance cover?

Public liability is helpful when faced with injury claims and compensation demands.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A client visits your premises and is injured in a slip or fall

- You visit a client site and damage equipment by knocking over a coffee or bumping someone’s desk

Other insurance consultants buy

If you're a consultant, the type of insurance coverage you need will vary depending on your circumstances. It's important to assess whether you have the financial means to replace or repair any computer equipment that might get damaged. You should also think about how you would handle a legal dispute and what steps you would take if HM Revenue & Customs conducts a tax audit.

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect consultants against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability.

At Suited, we combined £100,000 of commercial legal expenses insurance with helplines and other tools to better assist you in dealing with these issues, and it’s part of your subscription.

Commercial Legal Expenses offers qualified advice and assistance with:

- Legal and accountancy matters concerning your business

- Criminal prosecution

- Compliance & regulation issues

- Unpaid invoices (over £200)

For example:

- HMRC flags you for an IR35 investigation

- You need legal help chasing a major unpaid invoice

- You need guidance on compliance issues for your business

Portable electronics insurance

When working as a consultant, electronic devices are often vital tools for your daily operations. However, the unfortunate reality is that these devices can easily be stolen, damaged, or lost, leading to costly repairs or replacements.

To mitigate this risk and ensure your business equipment is protected, it's a good idea to obtain portable electronics insurance.

Consultants we insure

Suited offers comprehensive insurance policies that cater to the needs of a wide range of consultants, including:

- Academic consultants

- Acoustic consultants

- Business consultants

- Career consultants

- Catering consultants

- Compliance consultants

- Customer services consultants

- Energy consultants

- Environmental consultants

- Ergonomics consultants

- Farming consultants

- Fisheries consultants

- Food consultants

- Franchise consultants

- Health & safety consultants

- Human resources consultants

- IT consultants

- Management consultants

- Marketing consultants

- Occupational health consultants

- Operations consultants

- PR consultants

- Quality assurance consultants

- Sales consultants

- Strategy consultants

- Sustainability and waste consultants

- Sustainability consultants

- Traffic and transport consultants

- and more..

Shopping for independent consultant liability insurance

It is worth keeping the following in mind whether or not you choose to use Suited consultant insurance to safeguard your business:

Cheap consultant insurance

When choosing consultant insurance, don't just focus on cost. Consider after-sales service and how easily you can reach your provider. Suited offers multiple contact options and fast responses.

The reputation of the insurer is important

When it comes to insurance, it's crucial to have coverage when you need it most. That's why at Suited, we only work with financially stable insurers who have an A+ rating for their payout reputation.

Many providers charge fees to amend or cancel

Beware of low initial prices that may hide additional charges for monthly payments, policy amendments, or cancellations. At Suited, we don't charge any other fees, and you can cancel your policy at any time without any additional payment.

Some policy wordings are restrictive or have a high excess

Some insurance providers may offer tempting prices, but they may not provide adequate coverage. However, Suited ensures that our professional indemnity and public liability policies have a £0 excess.

Common questions

Do I need insurance for a consulting business?

All businesses, no matter how small, have liabilities. This also applies to self employed professionals. Even when you provide your services on a pro bono basis, you should still protect yourself with some insurance.

Where can I get business insurance for independent consultants?

Insurance for independent consultants can be obtained from online providers such as Suited but if your industry is complex or niche, you may need to contact a broker.

Do consultants need employers’ liability insurance?

If you work alone, you don’t need this cover. However, if you use volunteers, contractors or have friends and family helping out, check your obligations.

Do consultants need professional indemnity insurance?

Consultants need professional indemnity insurance if a client, agency or the industry regulator insist on it. However, you may also wish to have it, whether or not required, because it protects you against claims of compensation for making a professional mistake.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.