What is freelancer insurance?

Freelancer insurance is not one product. It usually comprises several products that combine to meet the insurance needs of your freelancer business.

Professional indemnity insurance is helpful if you provide advice or use your skills to solve your clients’ problems. You may need public liability if you have face-to-face dealings with people and property during your business. You may need product liability if you are involved in making or distributing products. Portable electronics insurance is good if you rely on your work equipment.

Do I need insurance as a freelancer?

There are many reasons why freelancers should have some level of insurance. No matter how small, every business faces risks, and insurance can be a helpful safety net.

Risk of being sued

When you start working independently, you are at risk of being sued by your clients, members of the public or subcontractors if you’re using any. Several products exist to protect you from legal claims.

Losing valuable business equipment or assets

Freelancers sometimes need specific equipment, stock, or other assets to carry out their work. Losing any of these assets could result in loss of work or downtime.

Unable to work due to illness

As a freelancer, you must look after yourself, including thinking of times when you may be too ill to work.

What is freelance liability insurance?

Sole trader liability insurance is a broad term that covers various legal liability products such as public liability, professional indemnity, employers' liability, and commercial legal expenses insurance.

As a freelancer, it's important to have legal liability insurance to safeguard yourself against legal actions that may arise from your business activities. Depending on your specific business needs, you may need to purchase one or more types of liability insurance products.

Professional indemnity insurance for freelancers

Professional indemnity is a legal cover that defends you if you face a legal claim due to your work. It provides legal advice representation and pays compensation if due.

These legal claims can stem from a variety of scenarios. Poor communication is often one of them. Especially at the beginning, freelancers, keen to secure their first contract, tend to gloss over the finer details. Most times, it leads to misunderstandings and client dissatisfaction.

Poorly defined projects or work leaves room for negotiations, and some clients like to exploit the grey area to get you to deliver more for free or, worse, ask for their money back.

Sometimes, you will be working on similar client projects, and the tendency is to reuse some previous work. That occasionally gives rise to disputes with clients.

While working with clients, you may access sensitive information about their business or customer base. Even if it’s an accidental slip of the tongue in front of another client, giving trade secrets away can be very costly.

What does professional indemnity insurance for freelancers cover?

Professional indemnity protects freelancers from legal claims accusing them of wrongdoing due to your professional advice or work.

Cover includes:

- Failing your duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example:

- Your client alleges that your work failed to deliver expected results and they want their money back or they’re suing you to do more for free

- Your client claims compensation because they believe your work cost them money

- You’re accused of sharing a client's confidential information with an unauthorised party

- Your work or advice led to an injury or death

- As a freelancer you may encounter issues over who owns the rights to the work produced, leading to legal disputes.

- You said something wrong or acted in a discriminatory manner

Choosing a freelance professional indemnity insurance limit that's right for you

Selecting an appropriate professional indemnity limit for your freelancing work is not always obvious; consider the following:

- If you're part of a professional body, look for the professional indemnity limit recommendation or requirement.

- If you operate independently, consider the complexity of your work and the advice you give—the more complex your work, the higher the limit you might need.

- Think about what downside there might be if your advice goes wrong. How much might it cost to fix a problem?

- Some insurance providers offer as little as £50,000 of cover, which might be tempting as the price will be low. However, with the rising cost of legal services, ask yourself if this amount will go far enough to cover solicitors' fees and possible compensation.

Does professional indemnity insurance cover my freelancing activities worldwide?

Your professional indemnity policy's ‘territory or geographical limits’ and ‘jurisdiction’ sections specify if your freelancer insurance will respond when working in different countries.

Territory or geographical limits:

The territory or geographical limit specifies where you can virtually or physically deliver your services. For example: “Worldwide.”

Jurisdictional limit:

The jurisdictional limit specifies which legal jurisdictions your policy will defend you if you are sued. For example: “Worldwide excluding US and Canada.”

Contract governance:

Any contracts or agreements you enter into with your clients should specify the ‘governing law’ for that contract, which is the jurisdiction in which parties can seek legal remedy for breach of contract.

Avoid entering contracts not governed by your local jurisdiction and/or excluded by your freelancer professional indemnity insurance.

If you work with US and Canadian clients, you can reduce your risk by not entering contracts governed by US and Canadian laws.

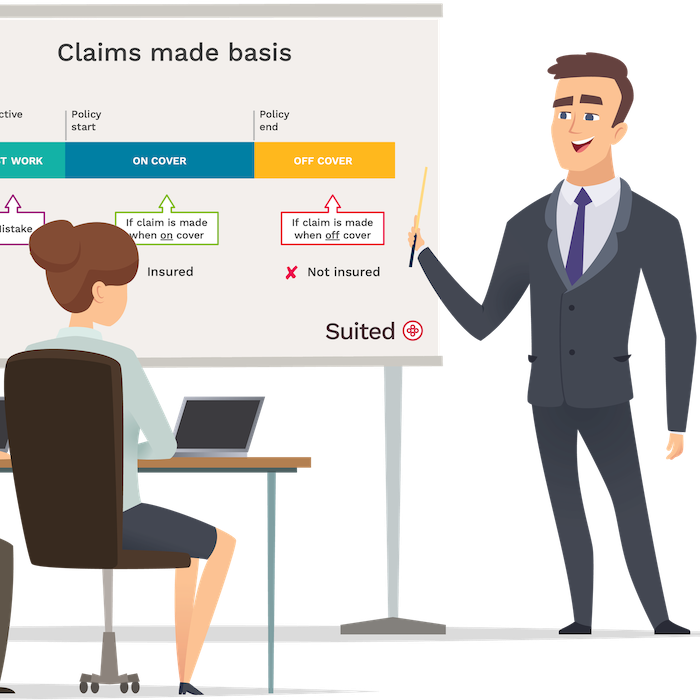

Switching your freelance professional indemnity insurance

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your freelancer insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I keep my professional indemnity if I take a break or retire from freelancing?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from freelancing. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of freelancing you did and the likelihood that a client might bring a claim against you.

Public liability insurance for freelancers

Public liability insurance is commonly needed by independent freelancers when their work involves physical contact with clients, the public or third-party property members.

Many freelancers meet clients at their homes, at their clients’ homes or in an office. Face-to-face meetings can expose freelancers to liability claims if a client trips or falls.

Freelance public liability insurance takes care of instances where an accident happened to a person or their property, and they seek compensation from you.

What does freelance public liability insurance cover?

Public liability provides legal defence and covers a possible payout if you're found liable for property damage or causing an injury.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A client visits you at your home or in your office and is injured in a slip or fall

- You have caused property damage while visiting your client’s property

- You have failed to warn someone of a risk, and they injured themselves, e.g. a hidden step or low ceiling

Other insurance freelancers buy

As a freelancer, the insurance coverage you require will depend on your individual situation. Do you rely on expensive computer equipment for your work? What would occur if you couldn't work due to sickness? Are you able to handle the responsibility of outstanding bills? Are you worried about the welfare of your family?

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect freelancers against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

Portable electronics insurance covers the cost of replacing or repairing business equipment, such as computers, cameras, or other tools of your trade. Freelancers are often reliant on all things electronic. Whether this equipment is yours or hired, you can insure the cost of repair or replacement should an accident happen.

Suppose you use a laptop or computer to store your clients' files or conduct video sessions; if this gets lost, damaged or stolen, this will cause significant work disruption and financial burden.

Shopping for freelance liability insurance

Whether or not you decide to use Suited freelance liability insurance to protect your business, it’s worth keeping the following in mind:

Cheap freelancer insurance

Cheaper insurance for freelancers may not be the best option. Consider the provider's after-sales service and ease of communication. Suited offers multiple communication options and prompt responses.

Select a fitting business activity description

When shopping for professional covers such as freelancer professional indemnity and public liability, ensure that you accurately select what you do for a living. Otherwise, you may end up with a product not designed for your profession.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no other fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

Some providers will offer attractive prices, but it is at the expense of cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Can I get income protection insurance for freelancers?

Some insurance providers do consider freelancers. If you are interested in this cover, check out our partners page.

What insurance do I need as a freelancer?

As a freelancer you may need several types of insurance. The types very much depend on your profession. But every active freelancer usually needs some liability insurance.

Do freelancers need employers’ liability insurance?

If you freelance alone, you don’t need employers’ liability insurance. However, if you use volunteers, contractors or have friends and family helping out, check your obligations.

Where can I buy the best insurance for freelancers?

The best insurance for freelancers is the one that protects from the risks associated with your work. Shop around and read about the covers on offer. Keep an eye on hidden costs - APR, charges to change or cancel.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.