Many self-employed professionals and small businesses are either confused about the term “claims made basis” or are completely unaware of its existence and impact.

We approached an expert on the subject, John Heaney, the CEO of Great American Insurance UK, and asked him to explain clearly what it means and how it all works.

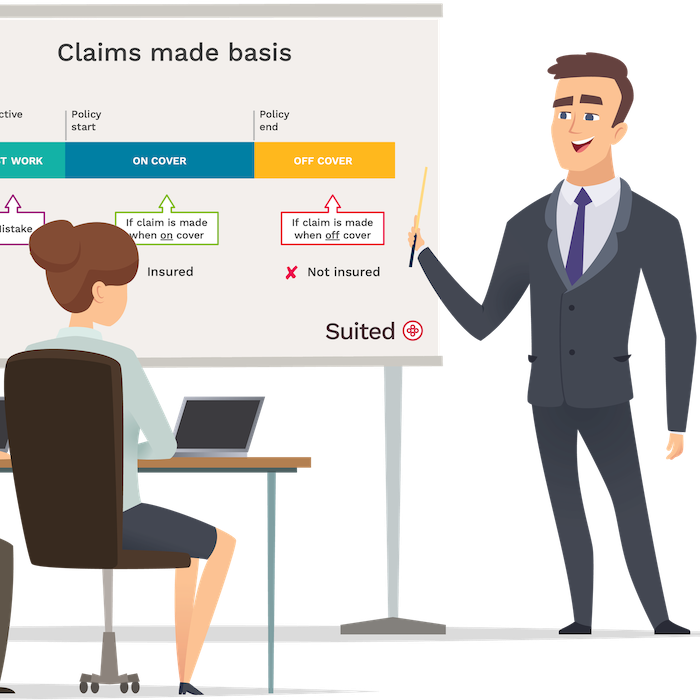

What does claims made basis mean?

An insurance policy issued on a claims made basis provides cover for any claims made against the policyholder during the period of insurance.

That can include claims made against the policyholder even if the incident giving rise to the claim happened before the current policy start date.

The caveat is that a claims made basis policy must be active when a claim is made. There is no cover if a claim is made after the policyholder cancels or lets their policy expire.

An example of a claims made basis policy

An excellent example of a claims made basis policy in the UK is professional indemnity insurance - one of the most required covers by self-employed professionals or businesses that lend their expertise and skills to solve their client's problems.

Key features of claims made basis policies

There are two key characteristics of a claims made basis policy:

- Coverage trigger: In a claims-made policy, cover is triggered when a claim is made against the insured and reported to the insurer during the policy period in which the claim is made. It is important to note that it does not matter when the alleged error, omission, or negligence occurred; what matters is the timing of the claim.

- Retroactive date: Claims-made policies often have a retroactive date, which is the date from which cover begins. Claims arising from incidents or events before this retroactive date may not be covered.

Professional indemnity insurance claims made basis

Most professional indemnity insurance in the UK works on a claims made basis. This means a professional indemnity claim must be reported to the insurer whilst the policy is active, AND the claim against the policyholder must have occurred during the period of insurance.

Why is professional indemnity on a claims made basis?

Professional indemnity claims made policies developed over time. One rationale for this approach is that claims arising from professional mistakes present themselves many months, sometimes many years later and it is often impossible to pinpoint the exact time of the incident. That is why professional indemnity insurance in the UK has been designed on a claims made basis.

What about claims resulting from past work?

A claims made policy doesn’t just cover incidents occurring during the current policy period. It can also respond to claims resulting from work delivered in the past, predating the start date of the current policy.

In order for a claims made basis policy to respond to claims resulting from past work, the policy must include two elements:

- Retroactive cover: a retroactive date is added to a claims made policy when it’s purchased. The retroactive date should go back far enough to provide cover for any work that may still give rise to a claim in the future. For example an architect may wish to set their retroactive date several years back.

- Past business activities listed under the current policy: if a claim resulting from past work is made against a policyholder, the type of work must be covered by the current policy. For example if a software developer has moved on to become an IT consultant, a claim from past work under the current policy may not be covered if the insured business activities do not list “software development”.

Claims made basis vs occurrence basis

We’ve already established that a claims made basis policy must be active when a claim is made and that it can cover incidents arising out of past and future work.

- Claims made basis: A claims occurring basis policy only provides cover for incidents occurring within the policy period. In other words, you cannot add a retroactive cover to a claims occurrence basis policy.

- Occurrence basis: On the other hand you can make a claim under an occurrence basis policy after it has expired or been cancelled as long as the incident giving rise to the claim occurred during the policy period.

Occurrence basis example

An example of an occurrence basis policy is public liability which is designed to respond to claims of property damage and injury. The time of these types of incidents are usually easy to determine. A claim might come after the policy has expired but it is still covered as long the date of the incident fall within the policy period.

Claims made basis example

Let’s take as example Paul - once upon time a software engineer who progressed his career to become an IT consultant.

Paul purchased a PI policy from 01.01.23 to 31.12.23. The business activities insured under the policy is that of an IT consultant. The policy does not include retroactive cover.

On 15.06.23 a claim is made against Paul for giving incorrect advice on 31.03.23 that led to a financial loss.. No problem, this is covered.

On 27.10.23 another claim is made against Paul, this time resulting from work completed on 15.04.21 in the capacity of a software engineer.

This is a problem for Paul. There is no cover for the second claim for two reasons. The current policy doesn’t include retroactive cover, i.e. cover for work done prior to the current policy start date. Nor does the current policy cover software engineering activities.

Remember you can’t make a claim under a professional indemnity policy that ended.

Can you make a claim under past claims made basis policy?

Paul can’t go to his previous insurers who used to insure his software engineering activities to make a claim. That policy expired and therefore no longer provides cover.

What Paul should have done when he switched professions is to include his past activities under the new policy and also add a retroactive cover.

This also applies when professionals and businesses are switching from one insurer to another in a quest for a better price. If they wish to stay insured for the past, they must ask the new insurance provider to include retroactive cover and list their past business activities.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.