What is bookkeeper insurance?

Bookkeeper insurance isn’t one product; it’s a combination of products designed to protect you and your business against legal threats and other risks.

Some professional bodies and client contracts may require bookkeepers to hold professional indemnity insurance. For example, ICB and AAT members may need to meet specific professional indemnity requirements. Always check the rules that apply to your membership, licence or client contract before choosing your cover limit.

If you meet clients face-to-face, you may also need public liability, and if your computer is essential to your work, you may want to add portable electronics.

Why do bookkeepers need insurance?

Even if you are a careful bookkeeper, mistakes can still occur. However, if one of these mistakes leads to financial loss for your client or triggers an investigation by HMRC, you may be accused of negligence and you could be held accountable for legal expenses or losses. That is why many bookkeepers choose professional indemnity insurance as the foundation of their business cover.

Accusations of costing your client money

As a bookkeeper, you handle your clients' finances. If a client believes your services cost them money, they may demand compensation.

Errors and omissions leading to your client getting fined

If a client feels they were fined due to your services, they may start proceedings against you.

Client injury during a face-to-face meeting

If you see clients face to face, there are always risks of trips, falls or property damage during meetings with you; this could result in legal proceedings against you.

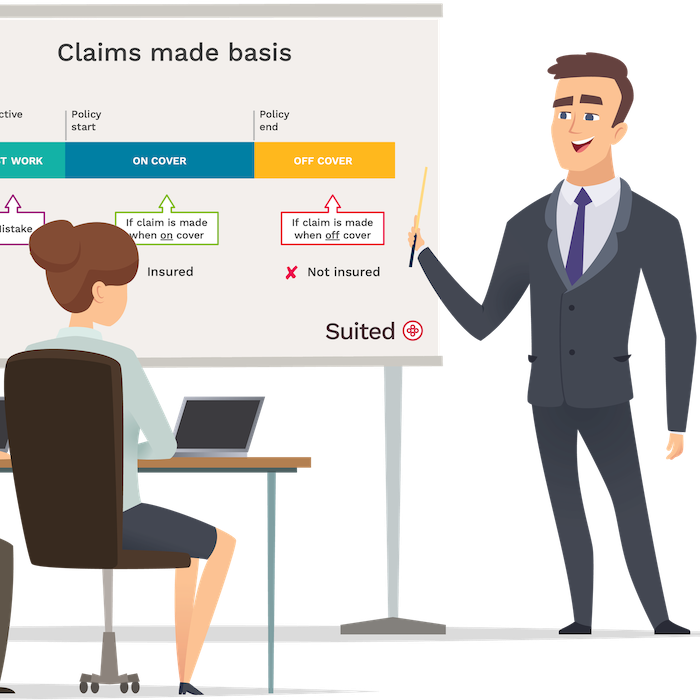

Professional indemnity insurance for bookkeepers

Professional indemnity is a legal cover that protects a bookkeeping business against accusations of professional errors and mistakes by unhappy clients.

Given the advisory nature of the bookkeeper profession, professional indemnity is the first insurance you should consider.

Learn more about the importance of bookkeeper insurance in our article: do bookkeepers need professional indemnity insurance?

What does professional indemnity insurance cover for bookkeepers?

Professional indemnity insurance provides financial protection and expert legal advice if you are in trouble with an unhappy client due to your bookkeeping activities.

Cover includes:

- Making an error

- Acting negligently

- Giving the wrong advice or recommendation

For example, you may be asked to pay compensation because:

- A client claims your professional advice led to a fine by HMRC

- A client believes your miscalculations cost them money

- You shared confidential information about your client with an unauthorised party

Suited professional indemnity insurance covers up to £2 million, backed by quality insurers and a dedicated legal team to assist if a situation arises.

The legal team is there at the early stages of a possible conflict with a client. They will advise you on how to proceed and help stop the issue in its tracks or limit damage. If the situation escalates, the legal team will also defend your case. The insurers pay for all legal costs.

Suited professional indemnity insurance comes with a bolt-on in the form of £100,000 legal expenses cover; this is useful for situations such as tax disputes, damaging PR crises or some other commercial legal issue your business faces.

How much professional indemnity does a bookkeeper need?

When starting in the bookkeeping business, there is sometimes the temptation to keep costs down by not investing in adequate liability insurance for bookkeepers. However, the price of a good PI cover is surprisingly low compared to just one hour with a solicitor whose help you would need if a client threatens legal action.

Factors to consider:

- The Institute of Certified Bookkeepers recommends cover of at least £50,000 or to select a limit which is at least a minimum of 2.5 times your annual turnover.

- How many employees or subcontractors do you have? The possibility of a professional mistake increases every time you delegate work to another person.

- How big is your most significant client account? Generally, the size of a client account goes hand in hand with its complexity and, therefore, the possible financial impact an error could cause.

- How many clients do you have, and what is the combined size? Sometimes, the same error or an incorrect procedure can be applied multiple times, causing a portfolio-wide issue.

- What is the most complex client account you look after, and what is the size of it? Complexity increases risk. If you specialise in more complex industries, ensure your insurance reflects this.

Switching your professional indemnity insurance

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your bookkeeper insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I keep professional indemnity insurance if I take a break or retire from bookkeeping?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from bookkeeping. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of bookkeeping you did and the likelihood that a client might bring a claim against you.

Public liability insurance for bookkeepers

It’s less common these days for bookkeepers to meet their clients face to face, but if you still work in a more personal way, you may wish to consider public liability.

Public liability cover protects bookkeepers and businesses against everyday accident such as spilling coffee over a client’s laptop or someone tripping during a meeting.

What does public liability insurance cover?

Public liability insurance responds to legal accusations of causing an accidental injury or property damage.

In the work environment of a bookkeeper, this is generally a low risk but still worth considering if you have regular face-to-face contact with your clients and third parties during your day.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

Someone may claim compensation because during a business meeting with you:

- They had a trip or fall at your home or business premises.

- By accident, you knocked over your client's expensive laptop.

- You failed to warn someone coming to your premises that there’s a step to mind, and they sprained their ankle.

Other insurance bookkeepers buy

If you work as a bookkeeper, the insurance coverage you require will vary based on your individual situation. Are you financially capable of replacing your computer equipment in case it gets lost, damaged, or stolen? Can you handle a legal conflict if it arises? Will you be able to pay for your business expenses if you fall ill?

Commercial legal expenses insurance

Commercial legal expenses insurance is designed to support professionals such as bookkeepers with a range of legal and tax-related matters that fall outside the scope of professional indemnity or public liability insurance.

This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

Accounting and bookkeeping are undergoing a tech revolution, which means the investment in electronic equipment has increased, and shoeboxes have been finally thrown out.

Suppose you have spent a considerable amount on your electronic equipment. In that case, you may like to protect it by having portable electronics insurance that would pay for the cost of damage or replacement.

Shopping for bookkeeper insurance

Whether you decide to use Suited for your bookkeeper insurance or not, it is important to remember the following:

Cheap bookkeeping insurance

Don't just settle for cheap bookkeeping insurance. Consider the level of after-sales service provided, which may be subpar. Ensure that you can easily reach your insurance provider when needed. At Suited, we offer multiple contact options and strive to provide prompt responses.

The reputation of the insurer is important

When it comes to insurance, it's crucial to have reliable coverage at crucial moments. At Suited, we only work with financially secure insurers who have an A+ rating, ensuring a solid payout reputation.

Many providers charge fees to amend or cancel

Beware of low initial prices that may conceal extra charges for monthly payments, policy amendments, or cancellations. Unlike other providers, Suited does not impose any additional fees, and you can cancel anytime without incurring any further costs.

Some policy wordings are restrictive or have a high excess

Be cautious of providers that offer tempting prices at the expense of adequate coverage. Suited offers both professional indemnity and public liability policies with no excess.

Common questions

Is professional indemnity insurance for bookkeepers compulsory?

Professional indemnity insurance for bookkeepers isn't compulsory but your customers or the association you are a member of may be expecting you to have PI cover in place.

Do I need bookkeeping insurance as a sole trader or freelancer?

You are not legally required to have bookkeeping insurance simply because you work as a sole trader or freelancer. However, professional indemnity insurance is often considered by bookkeepers because a client could make a claim if they believe a mistake in your work caused them a financial loss. Some clients, contracts or professional bodies may also require certain cover, so it is worth checking those requirements before buying insurance.

What insurance does a bookkeeper need?

Bookkeepers often consider professional indemnity insurance, which can help if a client claims they lost money because of a mistake in your work. Depending on how you run your business, you may also want to consider public liability, employers’ liability, legal expenses or business equipment cover. The right cover will depend on your work, clients, contracts and whether you have employees.

How is the cost of professional indemnity insurance calculated?

At Suited we only take into account your annual turnover, that's it. We do not charge per person.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.