What is insurance for nutritionists and dietitians?

Insurance for nutritionists and dietitians, often referred to as professional liability insurance or malpractice insurance, is designed to protect nutritionists from financial losses and legal claims that may arise in the course of their professional practice. It usually consists of professional indemnity insurance and may sometimes include other insurance covers depending on the practitioner’s activities.

Why do nutritionists and dietitians need insurance?

Nutritionists and dietitians meet clients who don't quite feel themselves and need someone else's guidance to get emotionally and physically better. This responsibility carries legal obligations and risks if things go wrong.

Compensation demands for adverse health effects

Nutritionists and dietitians provide dietary advice and recommendations to clients. If a client claims that the advice they received led to adverse health effects, such as allergies or nutritional deficiencies, the nutritionist may face a professional liability lawsuit.

Injury claims for harm caused by a recommended product

Many nutritionists sell or recommend dietary supplements and other nutritional products to clients. If a client experiences adverse effects or harm after using a recommended product and sues the nutritionist, product liability insurance can provide protection.

Loss of sensitive client information

Nutritionists frequently store sensitive client information electronically. In the event of accidentally disclosing something sensitive about a client, they may face legal claims related to privacy violations.

Medical bill claims following an accidental slip, trip, or fall

Nutritionists often meet with clients in their offices or other locations. If a client were to slip, trip, or fall during a consultation and sustain injuries, the nutritionist could be held responsible.

Professional indemnity insurance for nutritionists and dietitians

Most self-employed nutritionists benefit from the protection of professional indemnity insurance.

Professional indemnity is a legal cover that defends you if you face a legal claim due to your work. It provides legal advice and representation and pays compensation if due.

What does professional indemnity insurance for nutritionists and dietitians cover?

Professional indemnity protects nutritionists and dietitians from claims or accusations of wrongdoing from their professional advice.

Cover includes:

- Failing your duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example:

- A client claims your professional advice caused them harm

- You failed to give the correct direction to a client when you should have

- You shared a client's confidential information with an unauthorised party

- You acted in a discriminatory manner

- You caused offence

Choosing a nutritionist professional indemnity limit that’s right

Selecting a reasonable professional indemnity limit for your and dietitian work is not always obvious. Consider the following:

- If you're part of a nutritionist and dietitian organisation, they usually specify the professional indemnity limit they require—some need as high as £2,000,000.

- If you're an independent nutritionist, consider your level of qualification, experience, history of disputes with your clients, and the type of services you provide—the more complex your work, the higher the limit you might need.

- Think about what downside there might be if your advice goes wrong. How much might it cost to rectify?

- Some insurance providers offer as little as £50,000 of cover, which might be tempting as the price will be low. However, with the rising cost of legal services, ask yourself if this amount will go far enough to cover solicitors' fees and possible compensation.

Does professional indemnity insurance cover my nutritionist and dietitian activities worldwide?

Worldwide cover depends on the provisions in your particular counsellor insurance policy. When checking your professional indemnity insurance documentation, always look for the ‘territory or geographical limits’ and ‘jurisdiction’ sections.

The territorial or geographical limit defines where you can deliver your work - physically or virtually.

The territorial or geographical limit could be ‘worldwide’, meaning you can work with clients anywhere.

In contrast, the jurisdictional limit may say something like "worldwide excluding USA and Canada"; this means the policy will not protect you against claims brought against you in courts not included in or excluded by your policy.

This doesn’t mean that you can’t work with clients in the US or Canada. It just means that your client contracts should not be governed by those jurisdictions if you wish to reduce the risk of being sued in those countries.

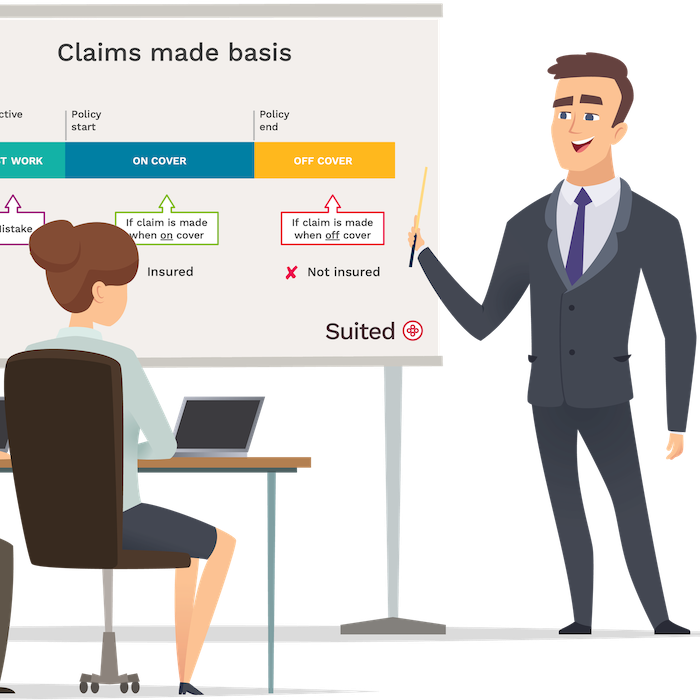

Switching your professional indemnity insurance

In the UK, most professional indemnity insurance is sold on a “claims made basis”; this essentially means two things:

- You must have an active policy at the time a claim is made, and

- The policy start date or retroactive date in your active policy must fall before the work in question was performed.

If your nutritionist and dietitian professional indemnity policy expires or is cancelled, you can no longer make a claim on it.

Therefore, if you change providers, make sure your past work is covered under your new policy. This is called retroactive cover.

Public & products liability insurance for nutritionists and dietitians

Public & products liability insurance may also be essential by independent nutritionists and dietitians, especially if they meet their clients face to face and recommend or sell products.

Public liability takes care of instances where your client may have had an accident and is now asking for compensation.

It can also be invaluable if the product you sold or recommended causes your client harm.

What does nutritionist and dietitian public & products liability insurance cover?

Public & products liability provides legal defence and covers a possible payout if you're found liable for property damage or causing an injury.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A client suffers a bad reaction taking one of your products and ends up in medical care.

- A client visits you at your home and is injured in a slip or fall

- While working with your client on a simple exercise routine, your client suffers an injury

What else should insurance for nutritionists and dietitians include?

Other covers depend on your circumstances. Do you own a laptop? Do you have employees? Do you have an office?

Portable Electronics insurance

Consider portable electronics insurance. Self-employed nutritionists and dietitians rely more and more on all things electronic. Whether this equipment is yours or hired, you can insure the cost of repair or replacement should an accident happen.

Commercial legal expenses

Commercial legal expenses insurance protects you and your business against commercial disputes, claims, criminal prosecutions, etc. It picks up issues not typically covered by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Shopping for nutritionist & dietitian liability insurance

Whether or not you decide to use Suited insurance for nutritionists and dietitians to protect your business, it’s worth keeping the following in mind:

Price isn’t everything

Some providers offer rock-bottom prices, but after-sales service could be lacklustre. Check how easy it is to get in contact with your insurance provider. At Suited, we offer several options and answer quickly.

The reputation of the insurer is important

Insurance needs to be there when you need it most. The payout reputation of an insurer is essential. Suited only uses financially sound insurers with an A+ rating.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no other fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

Some providers will offer attractive prices, but it is at the expense of cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Is professional indemnity insurance compulsory for nutritionists and dietitians?

Nutritionists and dietitians are not required to have liability insurance by law but it is wise to have it if you’re self-employed.

Will the work of my employees or subcontractors be covered by Suited nutritionist insurance?

Yes, any work by bonafide employees and contractually engaged third parties is covered by your Suited policy.

I’m returning to being employed again, can I cancel my Suited nutritionist insurance?

Yes, you can but before you do so consider whether you should maintain your professional indemnity insurance for a period of time. Claims are not always made against you straight away and without valid PI cover, you’re not protected. With Suited you can opt to hibernate your cover, meaning you pay less while staying insured for the past as long as you require.

Is professional indemnity insurance for nutritionists the same as nutritionist malpractice insurance?

Yes, these are two different names for the same insurance cover.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.