What is insurance for actuaries?

Insurance for actuaries can consist of several covers, but professional indemnity insurance is essential. The extent of your actuarial activities will determine the need for other insurance. For example, public liability might be needed if you meet other people during work. Business equipment insurance can be useful to cover any unexpected costs associated with theft or damage. Cyber cover is recommended for professionals and businesses that handle and store sensitive data.

Why do actuaries need insurance?

As an actuary, you apply your skills and expertise to develop financial and statistical theories designed to solve real business problems and reduce risk for your clients.

Legal protection from accusations of professional errors and omissions

Actuaries predict the future, and their clients rely on the advice. An error in the prediction can lead to substantial financial losses.

Contractual obligations

Clients often seek assurance that their interests are protected when they engage the services of an actuary. Having indemnity insurance in place is often a contractual must.

Financial stability

Professional indemnity insurance safeguards actuaries' financial stability. In the event of a significant claim, the insurance ensures that actuaries can continue their business operations without jeopardising their personal assets.

Data loss

Actuaries handle a lot of sensitive information and data. Sharing this information inadvertently with the wrong party can lead to compensation legal claims.

Professional indemnity insurance for actuaries

Professional indemnity insurance is a critical component of risk management for actuaries. It helps protect both their professional integrity and their financial well-being, ensuring that they can continue to provide actuarial services with confidence.

Actuaries are entrusted with financial and statistical responsibilities, and errors or negligence in their work can lead to financial losses for their clients. If a client believes that they have suffered a financial loss due to an actuary’s professional misconduct, they may file a legal claim.

What does professional indemnity insurance for actuaries cover?

Claims, even nuisance ones, can be expensive and time consuming to defend and the costs can be substantial. Even if a claim is unsuccessful, the time and effort involved in contesting it involves diverting otherwise productive resources.

PI insurance for actuaries provides cover for various liabilities and risks that actuaries may face in the course of their professional services. The specific coverage can vary based on the insurance policy and provider.

Cover responds to client accusations of:

- Breach of your duties

- Acting negligently

- Failing your duty of care

- Making an error

For example, a client or a third party may accuse you of:

- Miscalculating the pricing of investments or products

- Making an error in predicting the claims experience and profitability of a book of business

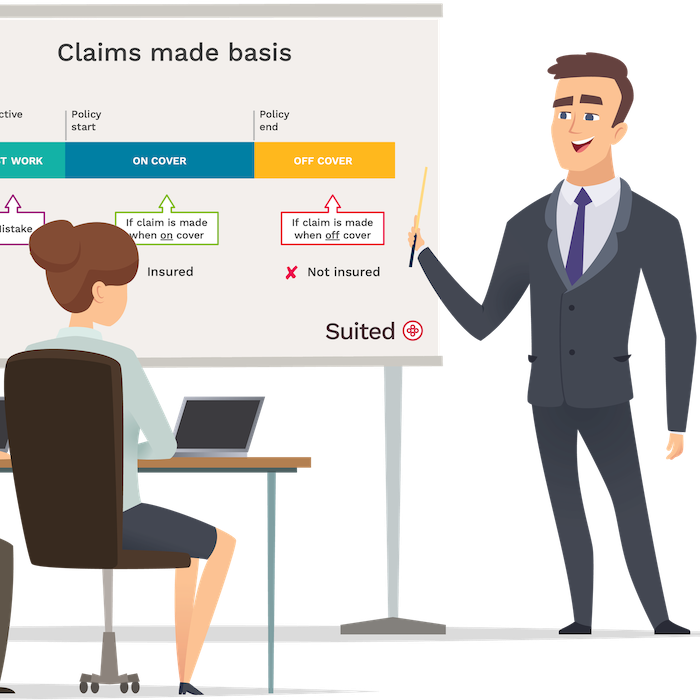

Switching your professional indemnity insurance

You may occasionally wish to consider a better deal. If you decide to switch to a new insurer, remember that you can no longer make claims against the previous policy. Ensure your past work is covered with the new insurers under what is called “retroactive cover.”

Should I keep professional indemnity insurance if I take a break or retire from being an actuary?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from providing actuarial services. Claims against professional misconduct can surface months or years after you delivered the work,

Remember: If you have cancelled your policy, your insurance will no longer work.

How long you keep your cover in place is up to you. Consider the type of work you did and the likelihood that a client might bring a claim against you.

Public liability insurance for actuaries

If part of your business activities is seeing your clients face to face, either at their premises or your office, you may benefit from having public liability insurance.

Public liability coverage safeguards your business from unforeseen incidents, such as accidentally spilling coffee on a client's expensive laptop or a client slipping on a wet floor. The expenses related to injury compensation and legal fees can rapidly escalate, potentially reaching thousands.

What does public liability insurance cover?

Public liability insurance addresses legal claims related to accidental injuries or property damage. In the context of an actuary’s workspace, the risk is typically low. However, it's prudent to contemplate this insurance if you engage in regular face-to-face interactions with clients and third parties during your daily activities.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

Someone may claim compensation because during a business meeting with you:

- They suffered an injury and blame you for causing it.

- You failed to warn someone coming to your premises that the floor is wet and suffered a nasty fall.

Other insurance actuaries buy

As an actuary, the insurance coverage you need will depend on your specific circumstances. Can you afford to replace your computer equipment if it's lost, damaged, or stolen? Are you prepared to handle a legal dispute if one arises?

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect actuaries against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability.

This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

Actuary services are often computer-dependent, and the cost of equipment has gone up. If you have invested in an expensive laptop, you may like to protect it by having portable electronics insurance that would pay for the cost of damage or replacement.

Common questions

I work with clients abroad; will my work be covered?

Suited professional indemnity insurance for actuaries covers work worldwide, but it will not respond to legal claims in US and Canadian jurisdictions.

Can Suited professional indemnity insurance cover my past work?

You can add retroactive cover with Suited. You can choose a date up to 6 years in the past.

Do I need to prove my qualifications before buying insurance with Suited?

You do not have to show relevant qualifications and/or experience to buy actuary insurance with Suited. However, you may be asked to provide this information during a claim situation.

I sometimes use subcontractors. Is their work covered?

If you use other actuaries on a contract basis, their work is covered as long as you have a contract. You should always insist that these contractors also have professional indemnity insurance.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.