What is self-employed hairdressing insurance?

Self-employed hairdressing insurance usually isn’t one thing. Hairdressers often purchase several products to meet the insurance needs of their work.

Because you’re working with people, public liability is often the first insurance most hairdressers buy, but hairdressers provide advice, so professional indemnity is also applicable.

Why do self-employed hairdressers need insurance?

Self-employed hairdressers work hard to make their clients look great, but accidents can still happen. Insurance can help cover any unexpected damages or injuries.

A client getting injured

Where scissors, chemicals and heat are used, an accident can happen anytime, no matter how careful and well-trained you are.

Advice goes wrong

A client is demanding compensation because a treatment you discussed during their last visit went wrong.

Something you said is taken out of context

Your business takes you to clients' homes, where everything becomes more personal. You may face a legal claim if you say something that is misinterpreted.

Receiving unfair chargebacks

Sometimes, an unhappy client might decide to claw back what they've paid you by initiating a chargeback. You'll need help to fight it if it is a substantial amount.

What is hairdresser liability insurance?

Hairdresser liability insurance is a term that covers several legal liability products, including public liability, professional indemnity and commercial legal expenses insurance.

Legal liability insurance protects hairdressers from legal claims arising from their work. Depending on how you work, you may need more than one liability insurance cover.

Public liability insurance for self-employed hairdressers

Public liability insurance protects hairdressers against accidents, injuries and property damage.

Self-employed hairdressers have up-close and personal contact with their clients. They also rent space at salons to cut hair and perform treatments. Both expose hairdressers to public liability claims if an accident happens.

What does hairdressing public liability insurance cover?

Suppose someone makes a claim against you for causing an accidental injury or property damage or loss. In that case, public liability insurance will provide legal defence and pay compensation if you become liable.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A wobbly chair or a hand slip causes an accidental injury to a client.

- You accidentally spill a chemical on your client’s expensive clothes or jeans.

- When standing up from the chair, a client trips and falls. They blame you for the accident and ask you to pay their medical expenses.

Professional indemnity insurance for hairdressers

Professional indemnity insurance protects hairdressers from claims or accusations of wrongdoing from their professional advice and services.

Professional indemnity insurance will immediately have your back if you receive an unhappy email, phone call or text threatening to sue you or demanding financial remedy.

Your insurers will appoint the appropriate legal aid to review your situation and advise you on what to do next.

What does hairdresser professional indemnity insurance cover?

Professional indemnity insurance will take over all communication between you and the client following a legal claim against your professional conduct. It will also pay compensation if you are found liable.

Cover includes:

- Failing your duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example, you may face financial demands from a client because:

- A client accuses you of ruining their hair, demanding monetary compensation.

- You may have said or done something that caused upset, and a client feels entitled to compensation.

What professional indemnity limit do hairdressers need?

The professional indemnity limit you need will reflect your particular hairdressing activities. When choosing a limit, consider how often you work, how many clients you have, and the possible financial impacts if your hairdressing advice or treatment goes wrong.

Switching your professional indemnity insurance

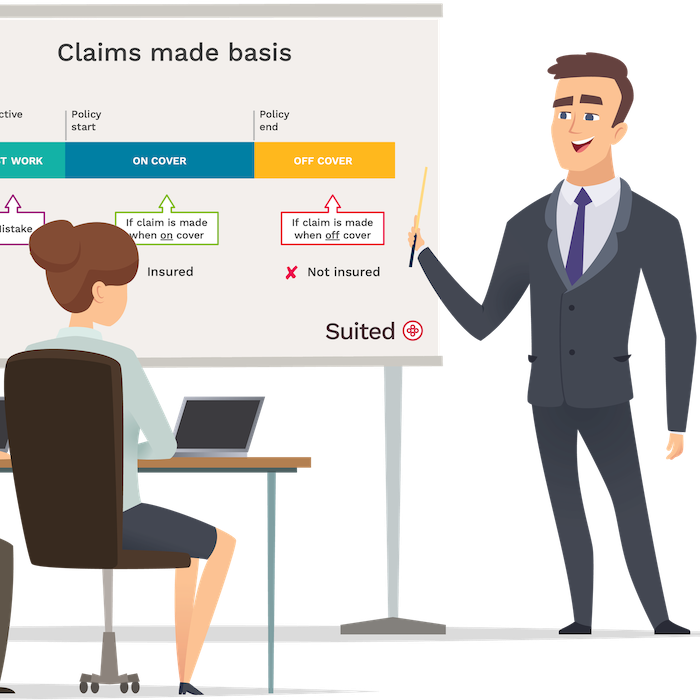

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your hairdressing insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I keep professional indemnity insurance if I pause or retire from self-employed hairdressing?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from hairdressing. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of hairdressing you did and the likelihood that a client might bring a claim against you.

Hairdresser professional indemnity - a case study

Hairdressers meet all kinds of people in their work, and while this is usually a perk of the job, there will always be people out there with less-than-honest intentions.

Just ask the north London salon who found themselves accused of burning a bald patch onto a client’s scalp back in 2017. The woman had damaged her scalp while dying her hair at home but tried to sue the salon for £30,000 over her self-inflicted bald spot.

Professional indemnity insurance is designed for this scenario. It covers the legal fees to fend off the rogue accusation, not causing a single penny to leave the business account.

A false allegation against you could result in legal fees eating into your hard-earned profits without professional indemnity insurance.

Other insurance hairdressers buy

As a hairdresser, the type of insurance you require will depend on your specific situation. Have you considered the possibility of a legal conflict? Additionally, how would you handle a tax-related problem? It's important to consider these factors when determining the insurance coverage you may need.

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect self-employed hairdressers against various tax and legal issues you may encounter due to your profession, which are not picked up by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Hair and beauty professionals we insure

Suited offers comprehensive insurance policies that cater to the needs of a wide range of hair and beauty professionals, including:

- Barbers

- Beauty consultants

- Hair stylists

- Makeup artists

- Manicurists

- Nail technicians

- Pedicurists

- and more..

Shopping for hairdresser liability insurance

Whether or not you decide to use Suited hairdressing insurance to protect your business, it’s worth keeping the following in mind:

Cheap hairdressing insurance

When choosing an hairdressing insurance provider, it's important to consider their after-sales service, even if they have low prices. You should check how easy it is to get in contact with them. At Suited, we prioritise our customers and offer multiple options for communication so we can quickly respond to any inquiries you may have.

The reputation of the insurer is important

Insurance needs to be there when you need it most. The payout reputation of an insurer is essential. Suited uses financially sound insurers with an A+ rating.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no extra fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

Some providers will offer attractive prices, but it is at the expense of cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Do self employed hairdressers need insurance?

Self employed hairdressers need insurance because the nature of their profession is to work very closely with their clients. As such hairdressers should consider business liability insurance to protect their reputation and bank balance.

What insurance does a self-employed hairdresser need?

The insurance a self employed hairdresser may need is professional indemnity insurance which protects from accusations of professional errors or misconduct and public liability insurance which shields from claims of injury or property damage.

What qualifications do you need to be a self employed hairdresser?

In order to obtain insurance with Suited you need to have demonstrable experience or qualifications.

What does it mean if a hairdresser is mobile?

Mobile hairdressers visit their clients at home. Often self employed hairdressers will do both, work in a salon but also provide mobile hairdressing services.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.