What is letting agent insurance?

Professional indemnity insurance for IT consultants can often be secured at a competitive price, with premiums influenced by factors such as the scope of your work, required coverage limits, annual income, and claims history. Below, you can explore the tailored covers Suited offers, along with their starting prices.

Professional indemnity protects letting agents from providing the wrong professional advice. Public liability covers accidents and injuries arising from face-to-face work. Commercial legal expenses insurance provides added legal protection. Portable electronics insurance is suitable to cover computers lost, damaged, or stolen.

Why do letting agents need insurance?

You strive to harmoniously bring a landlord and tenant together in a property ideal that suits them both. The issue is that often, it’s not that straightforward, and you may get caught in a legal dispute.

During a dispute, your professional conduct will come under scrutiny. Each party will be looking to blame the other for loss of earnings or incurred costs. As much as you can be confident that you provided the proper instructions and carried out all the right steps, there is always a chance that one of your clients will pursue a claim against you.

Regulatory compliance

While not directly required by law, professional indemnity insurance for letting agents is a must-have cover if you wish to operate in the UK property market.

Damage to property and snappy dogs

There are all kinds of pitfalls when showing other people's property. A pet running out of the door and causing damage or an injury is just one of many examples.

Failing to comply with regulations

You might have to comply with specific industry regulations as a letting agent. Even when you do everything right, you may face an enquiry into your conduct.

Claims of wrongdoing or overstepping the boundaries

You may find yourself at odds with either the tenant or the landlord. The tenant might feel that your behaviour is inappropriate, while the landlord can accuse you of not delivering the required service. Both could end up in a costly legal claim.

Professional indemnity insurance for letting agents

Most letting agents will require professional indemnity insurance.

Professional indemnity (PI) is a legal cover that defends you if you face a legal claim due to your work. It provides legal advice and representation and pays compensation if due.

Professional indemnity insurance for letting agents will pay for a legal expert to represent you, aid in redress, and compensate your client if your actions are deemed to have caused the claimant’s financial losses. Your client could be the landlord or the tenant; you have professional obligations to both.

Plus, professional indemnity insurance for letting agents is a regulatory requirement, and if you’re a member of a redress scheme, you are most likely required to have this cover.

What does professional indemnity insurance for letting agents cover?

Professional indemnity protects letting agents from claims or accusations of wrongdoing regarding their professional advice or work product.

Cover includes:

- Failing duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example:

- A client claims that you let their property to an unsuitable tenant, which led to a loss of rent

- A tenant may bring a claim against you for harassment

- One of your employees may have misappropriated client or tenant funds

- You acted in a discriminatory manner

Switching your professional indemnity insurance

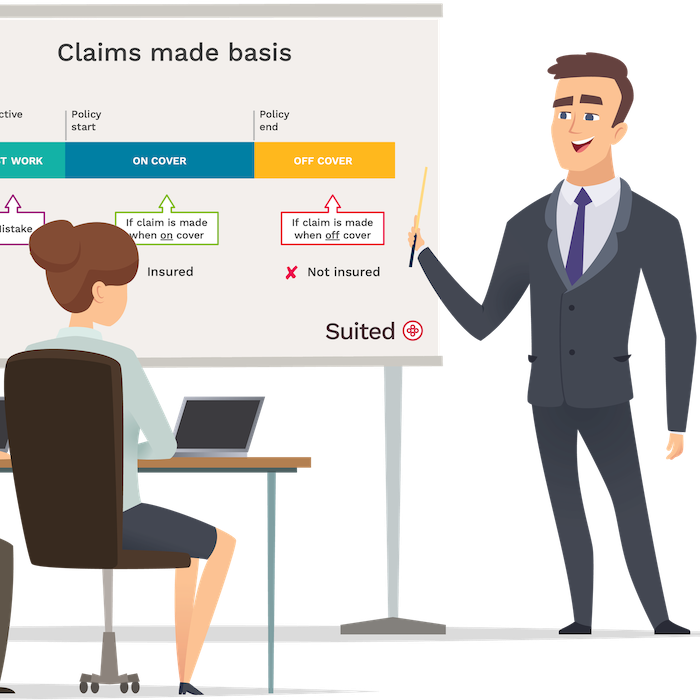

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your letting agent insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I keep professional indemnity insurance if I pause my letting activities?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from letting. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of letting work you did and the likelihood that a client might bring a claim against you.

Public liability insurance for letting agents

Public liability insurance is critical insurance for the majority of letting agents.

If you operate traditionally, i.e., hold your landlords' keys to show prospective tenants around, you should consider buying public liability insurance.

Public liability is a legal cover designed to protect letting agents from accusations of causing property damage or injury. Both do happen in the letting world and for saving a few pounds a month, it’s not worth exposing your business on this front.

What does letting agent public liability insurance cover?

Public liability provides legal defence and covers a possible payout if you're found liable for property damage or causing an injury.

Cover includes:

- accidental injury or death

- accidental property damage

For example, you may be sued because:

- During a property visit a prospective tenant knocks over a valuable piece of equipment or art

- While you see a landlord at their property, you accidentally ruin the new carpet by knocking over a cup of coffee

- You fail to warn a tenant of a hazard (a step, low ceiling or an unfenced pool) and they injure themselves

Other insurance letting agents buy

Other insurance letting agents require depends on your circumstances. Could you afford a legal battle? Would negative PR affect your reputation? Do you rely on expensive computers? How would you cover your business running costs if you fell ill? Do you have employees?

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect letting agents against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

Portable electronics insurance covers the cost of replacing or repairing business equipment, such as computers, cameras, or other tools of your letting agency. Gadgets for letting agents are getting more sophisticated and therefore quite costly to repair or replace.

Employers’ liability insurance for letting agents

If you have employees, you may be required by law to hold employers’ liability insurance; you could face a fine if you don't.

Shopping for letting agent liability insurance

Whether or not you decide to use Suited letting agent insurance to protect your business, it’s worth keeping the following in mind:

Cheap letting agent insurance

When selecting a letting agent insurance provider, it's essential to consider more than just the cost. It's crucial to assess their customer service as well. At Suited, we provide straightforward methods to reach us and prompt responses.

The insurer's reputation is essential

Insurance needs to be there when you need it most. The payout reputation of an insurer is critical. Suited only uses financially sound insurers with excellent ratings.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no other fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

A high policy excess can be an issue if it’s above the property ombudsman’s guidelines. Some providers will offer attractive prices, but it is at the expense of the cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Do letting agents usually have insurance?

They should and our recent survey into this profession shows that majority do even though they may not always understand how it can help.

Is professional indemnity insurance required by law for letting agents?

It isn’t but if you’re doing things properly, you should have this type of policy in place.

How much does PI insurance for letting agents cost?

Your cost will depend on your claims history, limit required and income.

What insurance do letting agents need?

Apart from what is already mentioned above, a letting agency might also need premises insurance, business interruption, cyber cover, commercial car insurance, and possibly key person insurance. It all depends on the specific circumstance of a business.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.