What is sports therapy insurance?

Insurance for sports therapists isn’t typically a single insurance product. It generally consists of two or more products to address the individual insurance needs of a sports therapy practice.

Most sports therapists will require both professional indemnity and public liability insurance as a minimum to protect themselves against the risks of their profession. Other covers will depend on your individual situation.

Why do sports therapists need insurance?

If you are a sports therapist and registered with a professional body, you will be typically required to have certain types of insurance.

Even if you are not registered, practising sports therapy without liability insurance is risky. Sports therapists offer services to clients who have a physiological problem. If the issue worsens rather than improves, you may be blamed and asked for compensation.

Making an injury worse

Sometimes, despite your best endeavours, a client may claim your sports therapy treatment or advice worsened their condition.

Blame for loss of earnings

If a client alleges your treatment made their injury worse and resulted in being unable to work, they could ask you to pay for their loss of earnings.

Accusations of failing duty of care

Clients meet you in private settings and expect a professional code of conduct. They may make a legal claim against you if they feel you've acted unprofessionally.

Unfortunate accidents

As a sports therapist, you will be using certain equipment and either have clients coming to you or visiting them at home. There are plenty of scenarios where an accidental fall or slip could end up in a claim against you.

The threat of being struck off

Even when not at fault, a complaint from a client or colleague may result in you being struck off a registered list of approved providers; in some cases, this may cost you your career.

Professional indemnity insurance for sports therapists

Professional indemnity insurance protects sports therapists from accusations of professional mistakes, negligence, failing duty of care, etc.

Professional indemnity insurance offers qualified legal assistance to defend your position, regardless of fault.

In the event that compensation is likely, the insurance will also cover the costs. Professional indemnity cover is usually required by professional bodies and it is also essential for receiving referrals from insurance companies and other business partners like GPs.

Occasionally, you may encounter the term 'medical malpractice insurance for sports therapists.' Essentially, this is just an alternative name for professional indemnity insurance tailored to sports therapists.

What does sports therapy professional indemnity insurance cover?

Professional indemnity insurance protects sports therapists from claims or accusations of wrongdoing from their professional advice or work product.

Cover includes:

- Failing your duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example:

- Your client alleges that your treatment failed to deliver expected results, and they want their money back, or they’re suing you to do more for free

- Your client claims compensation because they believe your work led to further injury preventing them from work

- You said something wrong or acted in a discriminatory manner

What professional indemnity limit do sports therapists need?

The professional indemnity limit you need for your practice should reflect the size and nature of your business.

Consider the following:

- Are you a member of a professional body that requires professional indemnity? If so, do they specify a necessary limit of liability?

- How many clients do you treat in your practice?

- Do you work with partners?

- What could the financial impact be if one or more treatments go wrong?

Generally, the more extensive and complex your sports therapy practice, the higher the limit you will need.

Switching your professional indemnity insurance

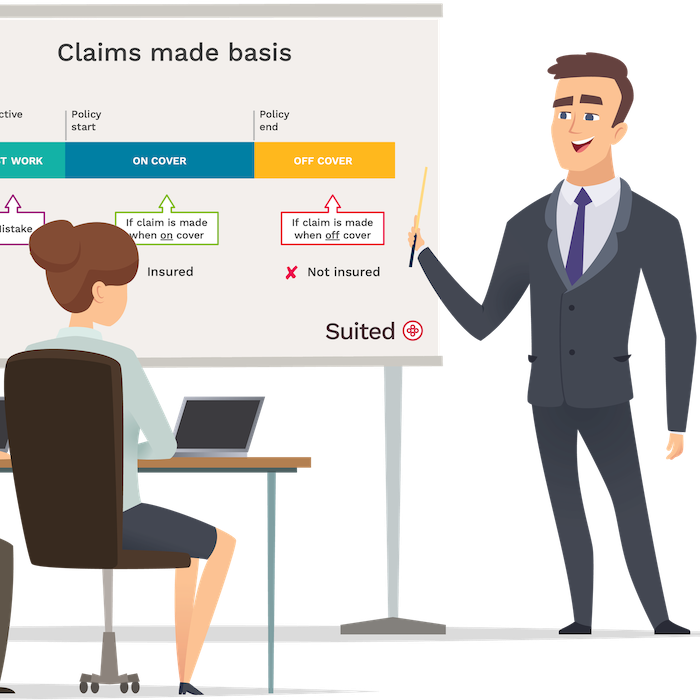

In the UK, most professional indemnity insurance is sold on a “claims-made basis”. This essentially means two things:

- You must have an active policy at the time a claim is made; and

- The policy period on your active policy must cover the time when the work was performed

When you cancel your professional indemnity policy, you can no longer make claims against that policy.

If you change provider, ensure your past work is covered by adding what is called “retroactive cover”.

Should I keep professional indemnity insurance if I close my sports therapy practice?

It’s wise to keep your professional indemnity if you close your sports therapy practice. Claims against sports therapists for professional misconduct or malpractice can surface months, sometimes years after you deliver the work.

If a past client sues you for damages and you have cancelled your professional indemnity, you will not be covered.

How long you keep your cover in place is up to you; consider the type of work you did, how long you worked and the likelihood that a client might bring a claim against you.

With Suited, you don’t have to pay full price if you no longer work as a sports therapist. You can hibernate your policy, allowing you to stay insured for past work at a much-reduced cost. You can leave your policy in hibernation as long as you like.

Public liability insurance for sports therapists

Public liability insurance covers risks faced by sports therapists in their face-to-face work.

Nearly all sports therapists see clients in person, so it’s wise to have a public liability insurance policy.

Public liability is an inexpensive cover that responds to claims of causing accidental harm to someone or their property. That someone could be your client, but it could also be a third party you come in contact with during your work.

What does sports therapy public liability insurance cover?

Public liability insurance is valuable when faced with injury claims and compensation demands.

Cover includes:

- accidental injury or death

- accidental property damage

For example

- A client visits your premises and is injured in a slip or fall, demanding financial compensation

- A client may accuse you of causing damage in their home. Even if you believe it wasn’t your fault, you may still end up with a compnesation demand.

Other insurance sports therapists might need

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect you against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability.

At Suited, we combined £100,000 of commercial legal expenses insurance with helplines and other tools to better assist you in dealing with these issues, and it’s part of your subscription.

Portable Electronics insurance

Sports therapy is getting much more technical, and some equipment can be costly.

If damaging or even losing an expensive piece of equipment would financially strain your bank balance, consider reducing the risk with portable electronics insurance.

Shopping for sports therapists liability insurance

Whether or not you decide to use Suited for your sports theraphy insurance, it’s worth keeping the following in mind:

Price isn’t everything

Some providers offer rock-bottom prices, but after-sales service could be lacklustre. Check how easy it is to get in contact with your insurance provider. At Suited, we offer several options and answer quickly.

The reputation of the insurer is important

Insurance needs to be there when you need it most. The payout reputation of an insurer is essential. Suited uses financially sound insurers with an A+ rating.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no extra fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

Some providers will offer attractive prices, but it is at the expense of cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Where does Suited insurance for sports therapists cover me?

You are covered whether you work from your premises, remotely, or visit your clients at their homes. If you provide services to clients based in the US or Canada, be aware that legal claims brought against you in those countries would not be covered.

My sports therapy treatments include dry needling and acupuncture. Will Suited cover those activities?

Unfortunately, at the moment, Suited cannot offer cover for any skin-penetrating treatments.

Do I need to submit evidence of my qualifications before buying the insurance?

Suited does not require any evidence of your qualifications, but we ask that you are fully qualified for your profession or in formal training by an accredited body. You may be asked to produce evidence in the event of a claim.

Does Suited offer insurance to sports therapy students?

Yes, Suited covers students in formal training with an accredited body or organisation.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.