Life coaching insurance

Life coaching can be personal, practical and wide-ranging. You may be helping clients think through career changes, confidence, relationships, goals, wellbeing or business decisions. Even when the work is positive and supportive, there is still a professional relationship between you and your client.

That is why many life coaches look for insurance that can respond if something goes wrong, a client complains, or a claim is made against them.

At Suited, we offer flexible insurance for UK life coaches, including professional indemnity, public liability, commercial legal expenses and business equipment cover. You can get a quote online, pay monthly and manage your policy without admin fees.

What is life coaching insurance?

Life coaching insurance is not one single type of cover. It usually refers to a combination of policies that can help protect life coaches against risks connected with their work.

For many life coaches, the main cover to consider is professional indemnity insurance. This is designed to help if a client alleges that your professional service caused them a loss.

Depending on how you work, you may also want to consider:

- Public liability if you meet clients in person, visit their premises or run sessions at events, venues or shared spaces.

- Commercial legal expenses insurance, which may help with certain business legal disputes, unpaid invoices, tax enquiries or regulatory issues.

- Business equipment cover, if you rely on laptops, phones, tablets, cameras or other equipment to run your coaching business.

- The right combination will depend on the type of coaching you provide, how you work with clients and any requirements in your contracts.

Do life coaches need insurance?

Life coach insurance is not usually a legal requirement in the UK. However, in our view, it is worth considering if you provide coaching, mentoring, personal development support or guidance to clients.

We often see life coaches looking for insurance because they want to protect themselves against complaints, disputes or allegations connected with their professional work. You may also be asked to hold insurance by corporate clients, venues, membership bodies or contract partners.

For example, a client may allege that:

- your coaching caused them financial loss

- you gave poor guidance or failed to deliver what was agreed

- confidential information was mishandled

- your service did not meet professional expectations

- something said during a session caused harm or distress

- they were injured during an in-person session or event

Not every complaint will be valid, and not every situation will be covered by insurance. But even where you have done nothing wrong, responding to a formal complaint or legal demand can take time, money and professional support.

Professional indemnity insurance for life coaches

Professional indemnity insurance for life coaches is designed to help with claims alleging professional negligence, mistakes, poor advice, breach of confidentiality or failure to deliver a professional service.

This can be relevant for life coaches because clients may rely on your guidance when making personal, career, business or lifestyle decisions. If a client later says that your coaching caused them a loss, professional indemnity insurance may help with legal defence costs and compensation where the claim is covered by the policy.

In our experience, professional indemnity is often the cover life coaches ask about first, especially where they work with corporate clients, professional bodies, training providers or coaching platforms.

What can life coaching professional indemnity insurance cover?

Professional indemnity insurance may help if a client claims that your coaching service caused them a loss or that you failed to act with reasonable care.

Examples could include allegations that you:

- gave poor guidance during a coaching session which led to loss of income

- you breached confidentiality which had a financial impact

- you made a professional mistake

- your client relied on your coaching and suffered a financial loss

Every policy has its own wording, limits and exclusions, so it is important to read the documents carefully before buying.

Is professional indemnity insurance required by coaching bodies or clients?

Some coaching bodies, corporate clients, venues and contracts may ask life coaches to have professional indemnity insurance in place before they start work.

This does not mean every life coach is legally required to hold professional indemnity insurance. It means the requirement may come from a client, membership organisation, training provider, venue or contract.

If you are arranging cover because someone has asked you to have insurance, we’d suggest checking:

- the type of insurance required

- the minimum limit of indemnity

- whether public liability is also required

- whether the policy needs to cover online and in-person work

- whether any specific wording or evidence of cover is needed

What about online life coaching?

Many life coaches now work online by video call, phone, email or messaging platforms. Professional indemnity insurance can still be relevant where your service is delivered remotely, because the main risk is often linked to the professional service itself rather than the location of the session.

If you work with clients outside the UK, you should check the policy’s territorial and jurisdictional limits. These sections explain where you can carry out your work and which legal jurisdictions the insurer may respond to if a claim is made.

For example, a policy may allow worldwide work but exclude claims brought under US or Canadian law. If you work internationally, this is worth checking carefully before you rely on the policy.

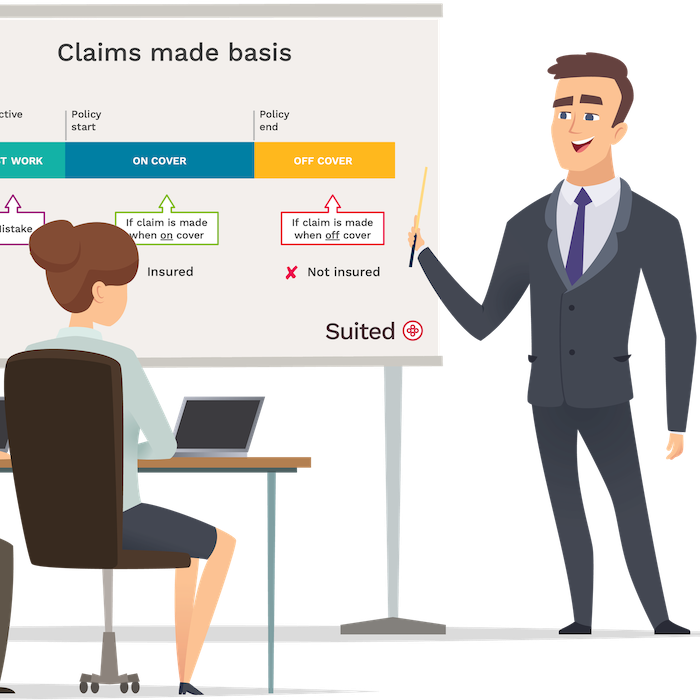

What if I switch professional indemnity insurance provider?

Professional indemnity insurance is usually written on a claims-made basis. This means the policy generally needs to be active when the claim is made, not only when the work was carried out.

If you switch provider, it is important to check whether your new policy covers your previous work. This is usually called retroactive cover. Without suitable retroactive cover, there may be a gap for work you completed before the new policy started.

Should I keep professional indemnity insurance if I stop coaching?

If you take a break from life coaching, retire or stop offering services, you may still want to think about whether past clients could bring a claim later.

Professional indemnity claims can sometimes arise months or years after the work was done. If the policy has ended by the time the claim is made, there may be no cover in place for that claim.

How long to keep cover is a personal and commercial decision. It may depend on the type of coaching you provided, your contracts, your client base and the likelihood of a future dispute.

Public liability insurance for life coaches

As a life coach or mentor, you see many clients face-to-face at various locations. Accidents sometimes happen and can lead to injuries or property damage. Public liability shields life coaches from claims of this nature and pays compensation if they become liable.

What does life coaching public liability insurance cover?

Suited public liability insurance is backed by an excellent insurer and a legal team provided by a specialised law firm should you encounter a situation with your client or a member of the public.

Cover includes:

Public liability protects you against legal accusations and compensation demands when either your client or a third party alleges that you have caused:

- accidental injury or death

- accidental property damage

For example:

Someone may claim compensation because during a session with you:

- You knocked over something valuable when visiting your client’s home

- You failed to warn them of a step, and they tripped and injured themselves

When might a life coach consider public liability insurance?

Sometimes, life coaches are under the impression that life coaching insurance isn’t necessary because they only volunteer or provide services to clients with whom they have a good relationship.

Just because you’re unpaid doesn’t mean you don’t still have professional responsibilities to those you coach. Your actions, whether paid or not, can still be questioned.

Whilst it may be challenging for your client to prove guilt and win compensation, you will still have to respond legally to any accusation. Legal action can be costly, with representation running into several hundred pounds an hour. Without professional indemnity insurance, you must fund any legal action from your pocket.

Other insurance life coaches buy

As a life coach, any additional insurance coverage you require will depend on your situation. Are you financially capable of replacing any lost, damaged or stolen computer equipment? Would you be able to handle a legal dispute if it arose? Would you be prepared to deal with a tax audit from HMRC?

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect life coaches against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

In today's world, life coaches rely heavily on various electronic equipment to deliver their services effectively. If your business is also dependent on such equipment, it is crucial to consider taking portable electronics insurance to safeguard your valuable tools against any potential damage or loss.

This insurance policy can provide you with the much-needed protection and peace of mind to continue providing top-notch services to your clients without any interruptions.

What life coach insurance may not cover

We think it is helpful to be clear that insurance will not cover every situation.

Depending on the policy wording, cover may not apply to:

- work outside the activities declared when you bought the policy

- services that should be carried out by a regulated professional

- counselling, therapy, medical advice, financial advice or legal advice, unless specifically agreed

- intentional, dishonest or criminal acts

- known disputes or circumstances that existed before the policy started

- claims brought in excluded territories or jurisdictions

- contractual liabilities that go beyond your normal legal responsibilities

If your work includes therapy, counselling, financial coaching, health advice, trauma support or other specialist services, we’d suggest checking carefully whether those activities are included.

What should life coaches check before buying insurance?

Before buying life coach insurance, we’d suggest checking whether:

- the policy covers the specific type of coaching you provide

- online, telephone and in-person sessions are included

- corporate coaching, executive coaching or group workshops are covered

- the insurer covers work with clients outside the UK

- the jurisdictional limits match your contracts

- past work is covered under the retroactive date

- any coaching body, client or venue requires a minimum level of cover

- the policy has an excess

- any exclusions apply to the services you provide

This is especially important if your work overlaps with counselling, therapy, wellbeing, HR, business advice, financial coaching or health-related support.

Buying life coaching insurance

Whether you choose Suited or another provider, we think it is worth looking beyond the headline price.

When comparing insurance for life coaches, you may want to check whether:

- the services you offer are actually covered

- professional indemnity is included

- public liability can be added (we find life coaches often change how they work and need the flexibility update their policy)

- you can amend or cancel the policy without admin fees

- how easy it is to contact the provider after you buy

- you can access documents, invoices and policy changes online

At Suited, we built our insurance to be flexible and easy to manage. You can pay monthly, make changes online, access your documents through your account and cancel without admin fees.

Get a life coach insurance quote

If you are a UK life coach, you can get a quote online with Suited in a few minutes. You can choose the cover that matches your business, review the policy documents before buying and manage your insurance through your online account.

Common questions

How much professional indemnity insurance does a life coach need?

The right limit will depend on your work, your clients, your contracts and any requirements set by venues, corporate clients or membership bodies. Some life coaches choose a limit based on contract requirements. Others consider the type of clients they work with and the possible cost of defending a claim. You should review the policy documents and choose a level of cover you are comfortable with.

What is the difference between professional indemnity and public liability for life coaches?

Professional indemnity insurance is designed to respond to claims connected with your professional service, such as allegations of negligence, mistakes, poor guidance or breach of confidentiality. Public liability insurance is designed to respond to claims involving accidental injury or property damage. For example, it may be relevant if you meet clients in person, visit their premises or run workshops.

Does life coach insurance cover online coaching?

It may do, depending on the policy wording. If you deliver coaching by video call, phone, email or messaging platforms, you should check whether remote work is included. You should also check the territorial and jurisdictional limits if you work with clients outside the UK.

Is life coaching a regulated profession in the UK?

Life coaching is not generally regulated in the same way as some professions such as solicitors, doctors or financial advisers. However, that does not remove the risk of complaints or claims. If your work overlaps with counselling, therapy, medical advice, financial advice or legal advice, you should check whether those activities are covered and whether separate qualifications, permissions or insurance are needed.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.