What is IT contractor insurance?

IT contractor insurance isn’t a single product; it’s a combination of products that meet your particular needs as an IT contractor.

IT contractors adopt many roles, but for any job, your contract will likely require you to have professional indemnity insurance. Public liability can also be a contractual obligation, and if you rely on your computer gear for your income, portable electronics insurance comes in handy.

Why do IT contractors need insurance?

Contract compliance

As an IT contractor, most engagements you enter into will stipulate in the contract that you must have and show proof of professional indemnity insurance.

However, being self-employed, you are ultimately responsible for any wrongdoing caused by your actions, so you should consider professional indemnity insurance more than just a box-ticking exercise.

Accusation of causing a financial loss

An unhappy client may allege your work product was substandard or resulted in a financial loss that they now want to recover from you.

IR35 enquiries and unpaid invoices

If you use an umbrella company or contract directly, you may be exposed to IR35 enquiries from HMRC. Regardless of how you're engaged, you still could be subject to late or non-payment of invoices.

Damage to your work equipment

You are likely to use your laptop or computer for your work. Could you afford the repair or replacement costs if that gets stolen or damaged?

IT contractor professional indemnity insurance

Professional indemnity insurance is the core insurance for all IT contractors. PI covers you against accusations of professional mistakes, negligence, and other claims against you caused by your work.

In the technology field, professional mistakes can lead to data leaks, system failures and project delays. If your error costs your client money, they may want to recover any financial loss from you.

Companies you contract with require you to have professional indemnity cover in case a professional mistake leads to a costly loss.

What does professional indemnity insurance for IT contractors cover?

Professional indemnity protects you from claims or accusations of wrongdoing from your professional IT advice or work product.

Cover includes:

- Failing your duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example:

- Your work is unfit for purpose, and your client refuses to pay your fee or is asking for a refund.

- An error or oversight on your behalf leads to a data loss, unauthorised sharing of personal data or GDPR breach. Your client is holding you responsible for the cost of remedy and compensation.

- Your work causes a significant system outage, leading to loss of sales, staff unable to work or reputational damage to your client.

What professional indemnity limit do IT contractors need?

Your work contract often dictates the minimum professional indemnity limit required.

If you have yet to receive your contract, ask your client or recruitment agency for the details so that you have enough time to explore your insurance options.

Check if the professional indemnity limit needs to be "any one loss" and how long you'll need to keep the cover in place after finishing the contract.

Limits

In the IT world, contracts usually require a specific amount, starting from £1,000,000 and going up to £10,000,000. The higher the limit, the higher the insurance cost.

Consider whether the required professional indemnity limit is appropriate for the work you will be delivering. You'd be surprised how often you can negotiate this part of your contract.

If your contract doesn't state that you require professional indemnity insurance but are keen to protect yourself, consider your level of input and responsibility for the project/programme.

The other thing to look for is any mention of liability in your contract; this clause should guide you to how much professional indemnity insurance you will need.

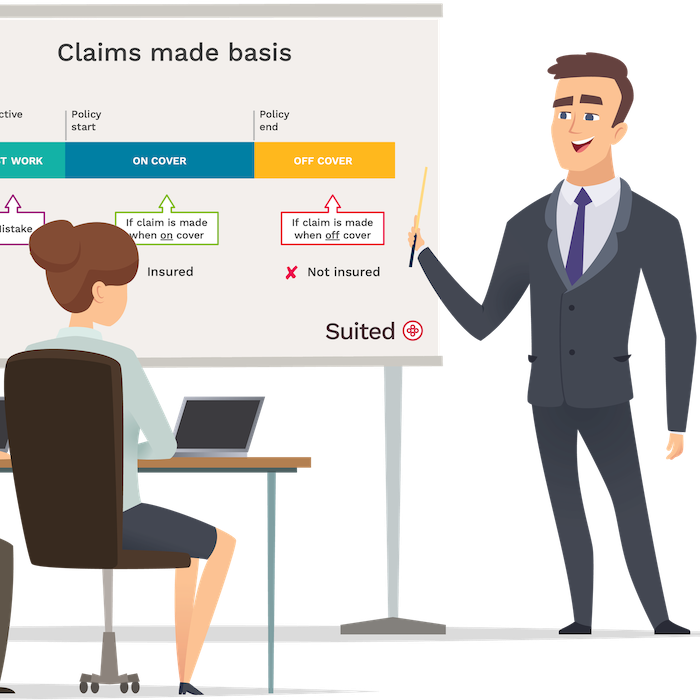

Any one loss vs. in the aggregate

IT contracts rarely stipulate whether the professional indemnity limit can or cannot be “in the aggregate”.

“In the aggregate” limit is a cover restriction, which means that irrespective of the number of claims you make during the period of insurance, you are only covered up to the policy limit across all claims.

For example, if you've bought a £1,000,000 PI policy and your first claim was £800,000, you only have £200,000 of PI cover remaining until your insurance renewal. Some IT contracts may require that your PI insurance is on an "any one loss" basis, which means your policy covers you up to the full policy limit per every claim.

Number of years

Some IT contracts require you to stay insured for up to 6 years after your contract finishes; you may be able to negotiate this for a shorter period.

Switching your professional indemnity insurance

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your IT contractor insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I retain professional indemnity if I am between contracts?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from IT contracting. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of IT contracting you did and the likelihood that a client might bring a claim against you.

IT contractor public liability insurance

In some cases, your contract may also require you to have public liability insurance.

Public liability protects you against accusations of causing an accident leading to an injury or property damage.

Public liability can be inexpensive protection against unfortunate incidents such as slips, falls, or you causing damage to a third party’s property.

What does IT contractor public liability insurance cover?

Public liability is helpful when faced with injury claims and compensation demands.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A client visits your premises and is injured in a slip or fall

- You visit a client site and damage equipment by knocking over a coffee

Other insurance IT contractors buy

If you work as an IT contractor, the kind of insurance coverage you need will vary based on your circumstances. Do you have the necessary financial means to replace or repair damaged computer equipment? Could you handle a legal dispute? What would you do if you had a tax audit by HM Revenue & Customs?

Commercial legal expenses insurance

Most commercial legal expenses insurance will protect IT contractors against various tax and legal issues you may encounter due to your profession, which are not covered by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

As an IT contractor, you likely depend heavily on electronic devices to complete your work. In the event that these devices are lost, damaged, or stolen, the cost of replacing them and maintaining your workflow could be significant.

To address this risk, it is wise to consider obtaining portable electronics insurance. Doing so can help you mitigate potential losses and get back to work as quickly as possible.

IT contractors we insure

Suited provides insurance coverage for a broad spectrum of IT contractors, including:

- IT project managers

- IT business analysts

- Computer programmers

- Systems analysts

- Database administrators

- Data architects

- Data recovery specialists

- IT infrastructure service providers

- IT network and systems engineers

- IT penetration testers

- and more...

Shopping for IT contractor indemnity insurance

When shopping for IT contractor insurance to safeguard your business, it's important to consider the following:

Cheap IT contractor insurance

When searching for IT contractor insurance, it's important to consider more than just the cost. The quality of after-sales service is crucial. Make sure to check how easy it is to reach your insurance provider. At Suited, we offer multiple contact options and respond promptly to ensure your peace of mind.

The reputation of the insurer is important

Insurance needs to be there when you need it most. The payout reputation of an insurer is essential. Suited only uses financially sound insurers with an A+ rating.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no extra fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

Some providers will offer attractive prices, but it is at the expense of cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Can I get my past work covered by Suited IT contractor insurance?

Yes, Suited offers a retroactive cover option. When buying your PI insurance, select the date from which you'd like to be covered and it will show on your policy schedule as the "retroactive date".

Will the work of my subcontractors be covered by Suited IT contractor professional indemnity insurance?

Yes, any work by subcontractors of your business is covered, however, do not waive your rights to hold them liable and you should insist that they have PI insurance.

Do IT contractors need public liability insurance?

That depends whether you come into a regular face to face contact with your clients, handle their property (computer hardware, etc) or deliver your services outside your usual place of work, for example at your client's premises. If any of the above applies to your business then you may wish to consider public liability insurance to additionally protect your business against any mishaps such as causing an injury or property damage.

How is the cost of IT contractor professional indemnity insurance calculated?

At Suited we only take into account your annual turnover, that's it. We do not charge per person.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.