While public liability insurance tends to be the better-known product for builders, professional indemnity insurance plays a very different role – one that could be critical if your work involves advice, design, or other professional input.

If you’re looking for a public and employer liability insurance quote, the good news is that getting covered online is easier than ever, especially if you run a small business.

For tradespeople, tools aren’t just equipment—they’re the lifeblood of your business. Whether you’re an electrician, plumber, carpenter, or builder, your tools enable you to get the job done.

IT contractors provide important services to businesses by developing software, managing IT infrastructure, and ensuring smooth operations. With these responsibilities come potential risks. When it comes to public liability insurance IT contractors are often contracctually required to buy it but is it always necessary, especially for those working remotely?

The recent case of Maya Meron, a violinist whose career ended due to an injury from a Pilates machine, underscores the critical importance of insurance for Pilates instructors and studios.

Find out what factors influence your architect PI insurance cost and whether you can save with Suited insurance for architects.

If you’re wondering if you need employers’ liability insurance for self-employed staff, the answer depends on how your self-employed staff are engaged.

Employers' liability insurance is not the same as professional indemnity - they are both a form of liability insurance, but that's where the similarities end.

Professional indemnity insurance provides peace of mind by covering you against potentially costly negligence claims.

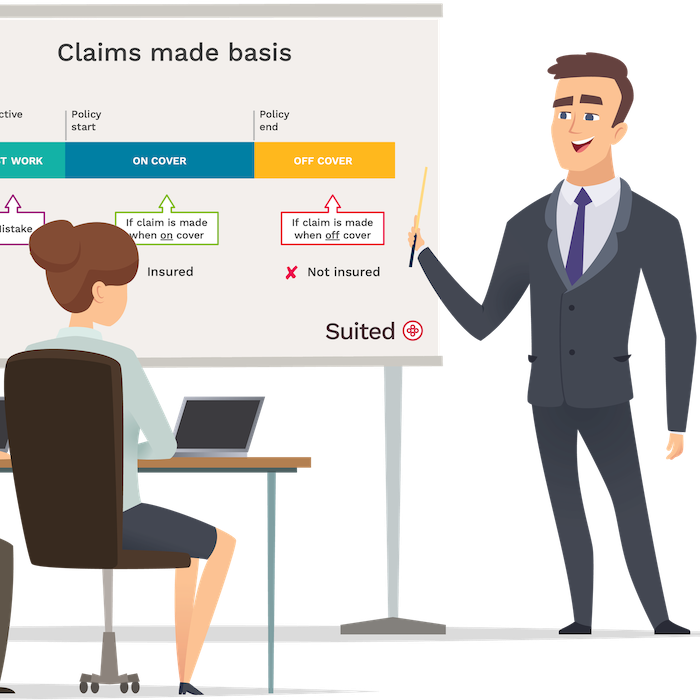

"Claims made basis" is a type of cover used by professional indemnity insurance. This policy type covers claims made and reported to the insurer during the policy period.

It’s possible but it’s not common, nor is it cost effective. When it comes to DJ liability insurance one day coverage tends to be relatively expensive because it is not what insurers like.

Freelancers and small businesses often say “I don’t need insurance, I’ve got no issues with my clients”. And hopefully that’s how it will always be for you. But every now and again something happens and client relations rapidly change. Just like it did for these business owners.

Just because you have set up a limited company in the UK doesn’t mean you need professional indemnity insurance. Your need for this type of cover is determined by whether your company is trading and what it does.

If you’re wondering if professional indemnity insurance is the same as public liability, the answer is no - they are both legal covers and protect you and your business against legal claims, but they mitigate different risks.

When it comes to start up business insurance costs UK insurance providers have the tendency to treat aspiring business owners with some caution.

For small businesses, liability insurance cost can start from as little as £80 a year but it can also rise to several hundreds. The average cost for a small business in the UK is around £220 - £350 a year. The price of liability insurance fluctuates based on the required insurance limits, industry, business size, and claims history.

Not quite literally but in this case study, a life coach’s livelihood, finances and peace of mind was certainly protected by having the good sense of purchasing life coaching insurance.

We have approached the claims department of Kennedys, a law firm that specialises in protecting bookkeepers and other professionals against accusations of wrongdoing, and asked whether they might able to share with us some recent experience of defending bookkeepers against a claim from an unhappy client.

Imagine you’ve just delivered the last piece of work for your client and plan to take some time off, perhaps for good. Cancelling your professional indemnity cover is an option but not a very good one.

A retroactive date in insurance is a line in the sand which determines a specific point in the past from which your insurers have agreed to insure your work.

We all come across this term "legal expenses cover" whenever we buy insurance, such as car or house insurance. The same happens if you search for business insurance and many have asked, is it worth the extra spend?